Tax Information

This section contains the annual tax guides provided by Spark Infrastructure and an ATO class ruling (CR 2022/22) to assist Securityholders to prepare their tax returns.

You should consult your tax adviser if you require tax advice on any of the issues contained in the tax guides or other documents on this website, or in relation to the completion of your income tax return.

Spark Infrastructure Group was acquired by Pika BidCo Pty Ltd on 22 December 2021. Pika BidCo Pty Ltd is a company indirectly owned by funds and/or investment vehicles managed and/or advised by Kohlberg Kravis Roberts & Co. L.P. and/or its affiliates, Ontario Teachers’ Pension Plan Board and Public Sector Pension Investment Board. It acquired 100% of the issued securities in Spark Infrastructure Group by way of a creditors’ scheme of arrangement, a trust scheme and related transactions (the Acquisition). As at the close of trade on 23 December 2021, securities in Spark Infrastructure Group were delisted from the Australian Securities Exchange.

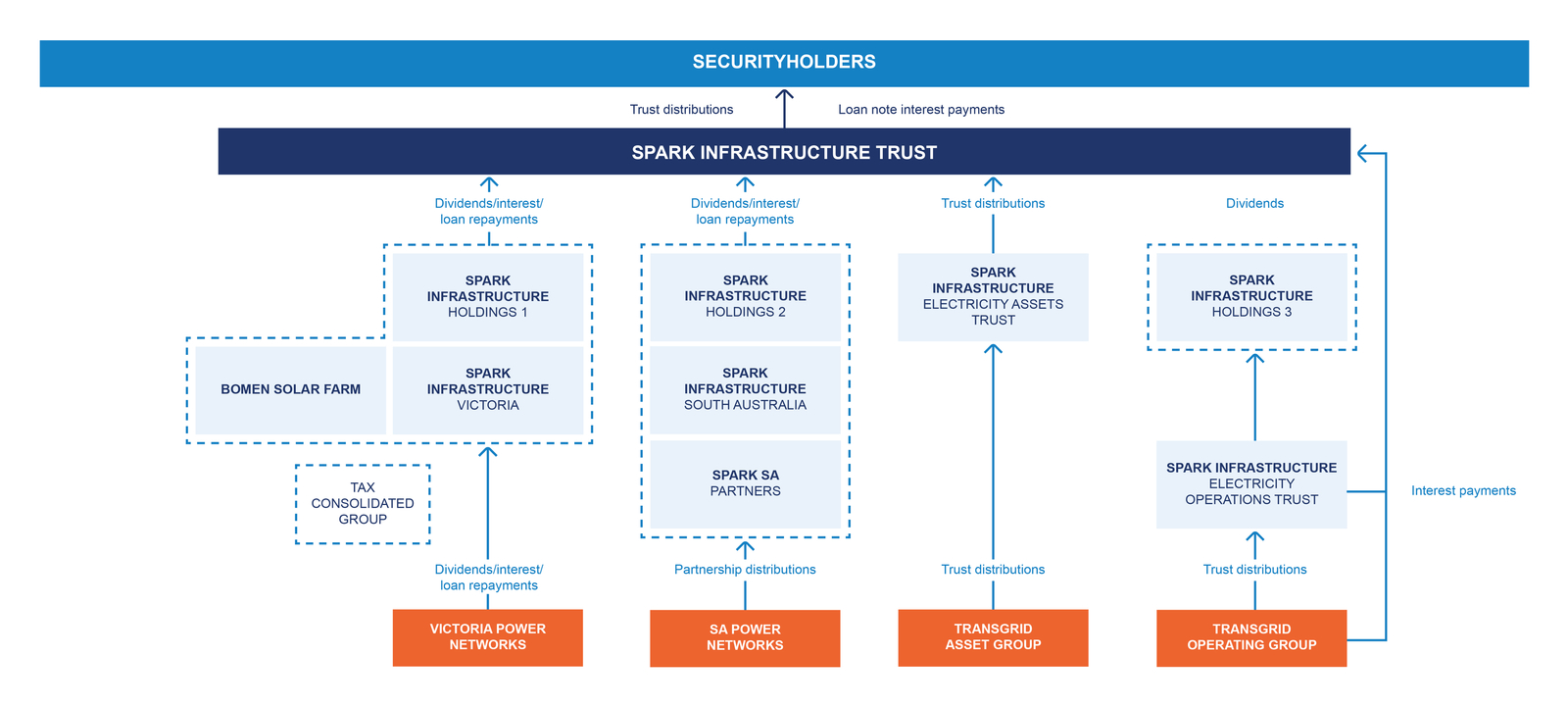

Spark Infrastructure structure pre 22 December 2021

Before the Acquisition, Spark Infrastructure securities comprised a Loan Note and a unit issued by Spark Infrastructure Trust. The structure of Spark Infrastructure before the Acquisition (i.e., pre 22 December 2021) is summarised in the diagram below:

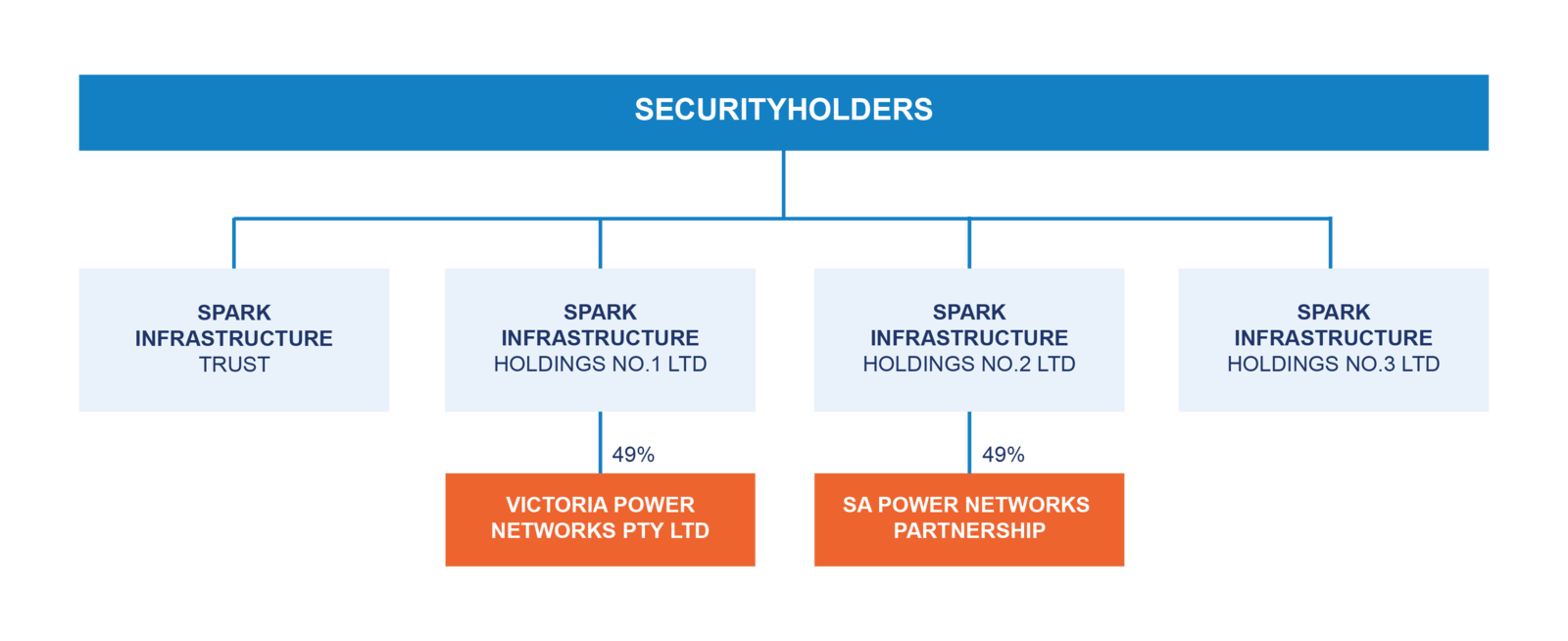

Spark Infrastructure’s structure pre 31 December 2010

Until 30 December 2010, Spark Infrastructure comprised four entities listed on the Australian Securities Exchange (ASX): Spark Infrastructure Trust, Spark Infrastructure Holdings No. 1 Limited, Spark Infrastructure Holdings No. 2 Limited, and Spark Infrastructure Holdings No. 3 Pty Limited (formerly Spark Infrastructure Holdings International Limited). Securities in these four entities and a Loan Note issued by Spark Infrastructure Trust were stapled together and could not be traded separately. The structure at 30 December 2010 is summarised in the diagram below:

The 2011 Tax Guide provides detailed information around the restructure of Spark Infrastructure, which was completed on 31 December 2010.